Understanding Supply and Demand is one of the most important parts of the JAIIB Indian Economy & Indian Financial System (IE & IFS) paper. Questions from this topic are regularly asked in the exam because it covers basic economic concepts like the law of demand, law of supply, equilibrium price, demand and supply curves, market equilibrium, and exceptions to the law of demand.

In this blog, we have provided detailed information on the topic of Supply and Demand. We have also included a free practice quiz PDF containing multiple-choice questions along with the correct answers and detailed explanations.

What topics are covered in the Supply and Demand Quiz?

The quiz is prepared according to the latest JAIIB IE & IFS syllabus and includes all major concepts that are important from the examination point of view.

| Topic | What You Will Learn |

| Demand | Meaning, utility, quantity demanded, demand schedule |

| Law of Demand | Relationship between price and demand |

| Demand Curve | Downward sloping demand curve and movement |

| Determinants of Demand | Income, price, preferences, population, expectations |

| Law of Diminishing Marginal Utility | Utility decreases with additional consumption |

| Supply | Meaning and factors affecting supply |

| Law of Supply | Direct relationship between price and supply |

| Supply Curve | Upward sloping supply curve |

| Market Equilibrium | Equilibrium price and equilibrium quantity |

| Shift vs Movement | Difference between movement and shift in curves |

| Exceptions to Law of Demand | Veblen Goods, Giffen Goods and Necessary Goods |

Download Practice Quiz on Demand and Supply

Strengthen your preparation for the JAIIB IE & IFS exam with a dedicated Demand and Supply Practice Quiz. The PDF covers important concepts such as the law of demand, law of supply, demand and supply curves, determinants, market equilibrium, movement and shift in curves, and exceptions to the law of demand.

Download PDF

Attempt Quiz on JAIIB IE & IFS Demand and Supply

Test your understanding of Demand and Supply with this practice quiz designed to improve your conceptual clarity. The quiz includes MCQs on demand, supply, equilibrium price, demand and supply curves, determinants, and frequently asked JAIIB concepts.

1. If a rise in the price of a commodity is accompanied by an increase in the quantity bought in the market, which of the following best explains this observation?

2. A household spends a fixed amount of Rs. 300 per month on rice (a luxury for it) and potatoes (an inferior good for it). If the price of rice rises, the household continues to buy the same quantity of rice but reduces its potato consumption. This phenomenon illustrates:

3. Which of the following pairs of goods would be classified as complementary goods?

4. An economy is currently at a price level where quantity supplied exceeds quantity demanded. What is the most likely subsequent adjustment in the market?

5. Which of the following correctly distinguishes a ‘shift’ in the demand curve from a ‘movement’ along the demand curve?

6. Why does the law of demand typically not apply to goods such as salt and life-saving medicines?

7. According to the law of diminishing marginal utility, as a consumer keeps consuming additional units of a good in a single sitting, the:

8. If the price of Nescafe rises while the price of Bru remains unchanged, which of the following is the most accurate outcome, assuming the two are substitutes?

9. A bank economist observes that during a sudden announcement of an impending lockdown, consumers’ purchases of groceries surge well before any change in price or income. This behavior is best explained by which determinant of demand?

10. Which of the following statements about Veblen goods is correct?

11. In which of the following situations would the supply curve of a commodity shift leftward, all else constant?

12. If the cost of raw materials, labour, and energy required to manufacture a good increases substantially, what is the most likely impact on the supply curve?

13. Two goods X and Y are substitutes in production (a firm can produce either using the same resources). If the price of X rises, what happens to the supply of Y?

14. At the equilibrium price of a commodity, which of the following is true?

15. If the price of a commodity is set below the equilibrium price (for instance due to a price ceiling), what is the most likely market outcome?

16. Which of the following changes would cause the demand curve for a normal good to shift to the right?

17. Which of the following would most likely cause the demand curve for an inferior good to shift leftward?

18. Consider a scenario where a bakery shop normally stocks 15 bread packets but currently has only 5 on the shelf, and the price has also risen. What does this combination of observations most likely indicate?

19. In the demand schedule for apples, as price falls from Rs. 500 to Rs. 100 per box, quantity demanded rises from 9 to 20 boxes, holding all other factors constant. This relationship represents which curve property?

20. Which of the following best explains why a price increase of a commodity discourages purchase through the ‘income effect’?

Quiz Summary

Final Score: 0.0

Sign Up

Login

Forgot Password

Please enter the Email ID we will send you a Email with the link to reset the password.

What is the law of demand?

The law of demand states that when the price of a product increases, its demand generally decreases. Similarly, when the price decreases, consumers tend to buy more of that product, assuming all other factors remain constant. This creates an inverse relationship between price and demand.

- Higher price leads to lower demand.

- Lower price leads to higher demand.

- Price and demand have an inverse relationship.

- Other factors like income and preferences remain constant.

- Represented by a downward-sloping demand curve.

What factors affect demand?

Demand is not influenced only by the price of a product. Many other economic and social factors also affect consumer demand. A change in these factors shifts the entire demand curve instead of causing movement along the curve.

- Price of the commodity

- Consumer income

- Population size

- Consumer tastes and preferences

- Prices of substitute goods

- Prices of complementary goods

- Weather and seasonal conditions

- Future expectations

- Cultural and social factors

Also: Check out the detailed JAIIB IE and IFS Syllabus

How is movement different from a shift in the demand curve?

Students often confuse movement and shift in the demand curve. Understanding this difference is very important because direct questions are asked in the JAIIB examination.

| Movement in Demand Curve | Shift in Demand Curve |

| Caused by change in price | Caused by factors other than price |

| Same demand curve | New demand curve |

| Quantity demanded changes | Entire demand changes |

| Law of demand applies | Determinants like income or preferences change |

What is the law of diminishing marginal utility?

The law of diminishing marginal utility explains that the satisfaction received from consuming additional units of the same product keeps decreasing. The first unit provides the highest satisfaction, while every additional unit gives comparatively less satisfaction.

- First glass of water gives maximum satisfaction.

- Second glass gives less satisfaction.

- Third or fourth glass provides even lower satisfaction.

- Continuous consumption may even reduce satisfaction.

What is the law of supply?

The law of supply states that producers are willing to supply more goods when market prices increase because they can earn higher profits. When prices fall, producers reduce supply.

- Price and supply have a direct relationship.

- Higher price increases supply.

- Lower price decreases supply.

- Represented by an upward-sloping supply curve.

- Producers focus on profit maximization.

Also Check: JAIIB IE and IFS Study Material

What factors affect supply?

Apart from market price, several other factors influence the quantity supplied by producers. These factors can shift the supply curve to the left or right.

- Cost of production

- Price of raw materials

- Technology

- Government taxes and subsidies

- Weather conditions

- Market expectations

- Availability of resources

- Prices of related goods

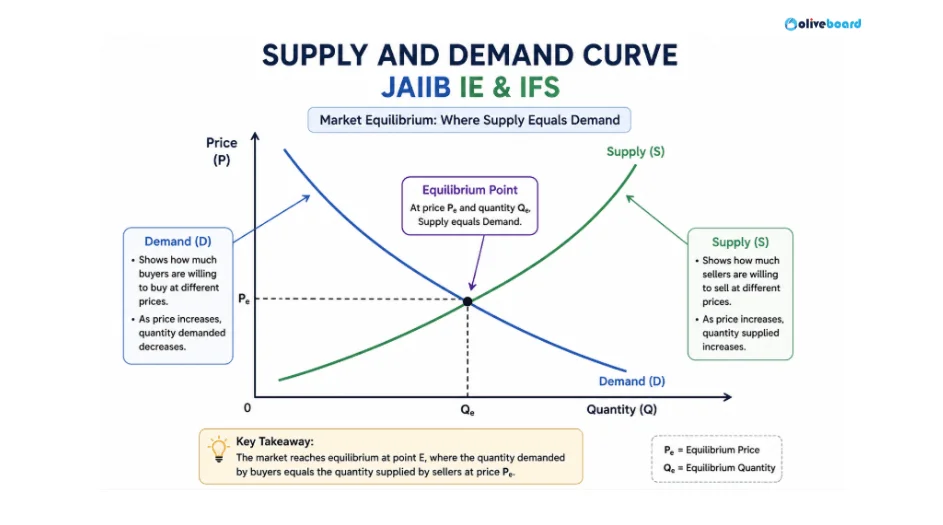

What is market equilibrium?

Market equilibrium is the point where the quantity demanded by consumers becomes equal to the quantity supplied by producers. At this point, the market reaches balance, and there is no pressure for the price to change unless other factors change.

- Demand equals supply.

- Stable market price.

- Stable quantity.

- No shortage or surplus.

- Price remains unchanged unless determinants shift.

What are the exceptions to the law of demand?

Although the law of demand generally applies to most products, there are certain situations where demand may increase even when prices rise.

| Exception | Explanation |

| Veblen Goods | Expensive luxury goods purchased for status and prestige |

| Giffen Goods | Inferior goods where demand increases despite a price rise |

| Necessary Goods | Essential goods like medicines and salt where demand changes very little |

| Increase in Income | Higher income can maintain or increase demand even when prices rise |

Why is equilibrium price important in economics?

Equilibrium price ensures that producers and consumers are both satisfied. It prevents excess supply and shortages in the market while maintaining price stability.

- Maintains market balance.

- Eliminates surplus.

- Reduces shortages.

- Helps efficient resource allocation.

- Indicates a stable market condition.

Also Check: JAIIB IE and IFS Mind Map PDF

How does the Supply and Demand PDF help in JAIIB preparation?

A downloadable PDF allows you to revise important concepts anytime without depending on internet access. It serves as a quick revision guide before mock tests and the final examination.

- Easy offline revision.

- Covers important formulas and concepts.

- Useful before the examination.

- Helps with last-minute preparation.

- Supports regular practice with the quiz.

FAQs

Yes, it is one of the important topics and frequently contributes multiple questions in the IE & IFS paper.

Demand is the quantity of a good or service that consumers are willing and able to buy at different prices.

The law of demand states that as the price of a product increases, its demand decreases, keeping other factors constant.

Market equilibrium is the point where the quantity demanded equals the quantity supplied, determining the equilibrium price.

The main determinants of demand include price, consumer income, tastes and preferences, population, and prices of related goods.

Hi, I’m Aditi. I work as a Content Writer at Oliveboard, where I have been simplifying exam-related content for the past 4 years. I create clear and easy-to-understand guides for JAIIB, CAIIB, and UGC exams. My work includes breaking down notifications, admit cards, and exam updates, as well as preparing study plans and subject-wise strategies.

My goal is to support working professionals in managing their exam preparation alongside a full-time job and to help them achieve career growth.